1740109648391-Accounting, Grade 11, Task1, Written Report, QP

Uploaded by

salmaessa081740109648391-Accounting, Grade 11, Task1, Written Report, QP

Uploaded by

salmaessa08Common questions

Powered by AITo calculate the bank account balance, consider all outstanding deposits and payments not yet processed, reconciliations for recorded errors, direct debits, and credits from the bank statement not yet recorded in the cash journals. For February 28, 2025, these could include pending EFTs and unrecorded bank charges .

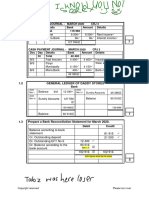

Preparing a bank reconciliation statement is important to ensure the accuracy of the business’s cash records and to identify any discrepancies between the company's cash account in its financial records and its bank statement. Discrepancies could arise from outstanding checks, deposits in transit, or errors in recording transactions, thus reconciling helps in detecting fraud or accounting errors and ensures that financial statements are accurate .

The vehicle's sale on credit is recorded by debiting the asset disposal account with the cost price of R190,000. A separate entry is made to transfer the accumulated depreciation of R171,000 to this account. The credit side of the asset disposal account reflects the sale price of R2,700, and any residual value or profit/loss is determined as the balancing figure in the asset disposal account .

To calculate depreciation on the vehicle sold, apply the 20% depreciation rate on the original cost price of the vehicle, which is R190,000. Since the vehicle was disposed of in December after holding it for nine months starting from March, the calculated depreciation for the year would be 20% of R190,000, pro-rated for the time period between March and December .

Good internal control over movable fixed assets includes regular physical counts to ensure assets are present and match records, and proper authorization procedures for asset acquisition and disposal to prevent asset misappropriation or unauthorized use .

Bank errors, such as an incorrect deposit amount, should be investigated and adjusted in the bank reconciliation statement. This involves correcting the error in the books to match the correct bank statement amount. For example, if an error of R9,200 was identified, this should be subtracted from or added to the relevant transactions in the reconciliation statement to reflect the accurate bank account balance .

EFT payments provide advantages such as increased efficiency and security. They allow for quicker transactions with fewer errors compared to manual processing, and they also provide a secure way of transferring funds directly between accounts, reducing the risk of cash theft or fraud .

Unbanked deposits, such as the R11,500 that was stolen, have a negative impact as they reduce available cash flows and potentially misstate asset balances. This must be accounted for as a loss, affecting both the income statement through expense recognition and the balance sheet through a decreased cash account, ensuring that financial statements reflect the true financial position .

The GAAP principle of 'Materiality' informs the bookkeeper to consider the significance of the transaction and its effect on the financial statements. In the case of the R11 500 deposit that was stolen, an entry should be made to write off the amount because not acknowledging it in the ledger could materially misstate the financial position of the business .

The vehicle was originally purchased on March 1, 2024. Since the depreciation on the vehicle sold started accumulating from that date and the accumulated depreciation was R171,000 as of March, it implies that the vehicle was held for full depreciation cycles from March 1 .